On Sat, Dec 24, 2011 at 7:12 PM, jack danials <cornmash007@yahoo.com> wrote:

--- On Fri, 12/23/11, rudi thomas <rudithomas1011@yahoo.com> wrote:

From: rudi thomas <rudithomas1011@yahoo.com>

Subject: The Securitization and Foreclosure Coverup Big Banks Are Hiding

To: "Jack Danials" <cornmash007@yahoo.com>

Date: Friday, December 23, 2011, 5:18 PM

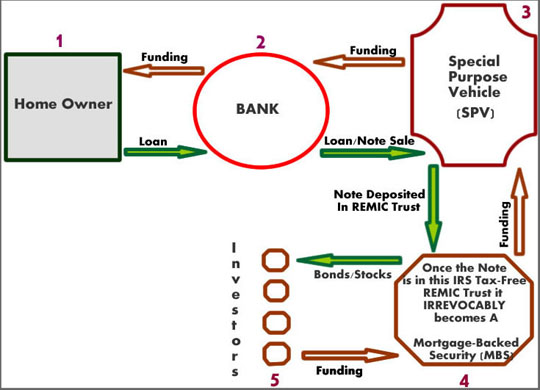

Step1. Homeowner receives loan from Bank-X. Step2. Bank-X sells the loan to SPV and is paid in full. Step3. SPV transfers note into REMIC trust and is paid in full by Trustees. Step4.The note is now a Security, the process is irreversible and complete. Step5. Investors (OWNERS) of the Certificates (Bonds/Stocks) receive payment from the REMIC Trust.Edited by Joseph Ernest February 14, 2011Written by Rondaben EsquireNewscast Media --The process of acquiring or selling homes in the past few years has been forever changed by the securitization process that has affected homes of over 60 million Americans. I receive many emails and questions regarding this topic, and since I am not an attorney, I will direct the readers to a brilliantly written article by Rodaben Esquire, that explains the whole process and by the end of the article, you'll be surprised as to what the banks are hiding from you. I have also created the chart above to show you the flow of transactions.Understanding Securitization and Foreclosure:Bank A issues a mortgage to Caprice to purchase a house. Two documents are produced, a promissory note and a trust deed. The trust deed is essentially the title of the property that is held in trust until the promise to repay the loan (promissory note) is satisfied. Once the loan is paid in full Bank A releases its claim on the Trust deed and ownership passes in full to Caprice. That is what most of us believe happens in mortgages because you are not informed as to what happens after the paperwork is signed and how it impacts the title and promissory note you are obligated to. This is intentional, and represents the entire scheme that allows securitization occur. If the process that is now used is too complex it can be used as a justification to allow the shenanigans that occur during a foreclosure process to happen while the judges and juries believe that the process described above is what is actually happening. Lets look next at the basics of securitization.Once the mortgage has been formed between Caprice and Bank A, Bank A wants to get rid of it as fast as possible and recoup its funds. To take advantage of this and the tax benefits of securitization it has to form what is called an SPV, a (Special Purpose Vehicle) Think of it as a shell company. This protects the mortgage if something happened and Bank A went out of business. The mortgage would still exist. It also theoretically reduces the liability of Bank A to the mortgage default. It is important to realize one important thing here…the two documents that Caprice signed (the promissory note and the title deed) are now SEPARATED. The trust deed remains with its trustee. The promissory note—the asset that pays money—is SOLD to the SPV. The original note is paid off by the SPV and the stream of payments becomes the property of the SPV. Bank A has its money in full and no longer has ANY interest in the mortgage.Now, the SPV forms a new trust entity. This trust entity is defined by the IRS as a REMIC (Real Estate Mortgage Investment Conduit) and must adhere to the laws regarding such a trust. The benefit of doing this is that when the SPV transfers the mortgages into the Trust NO TAXES MUST BE PAID ON THE TRANSFER. This makes the trust a much more efficient and profitable vehicle for investors. REMICs, in turn, cannot retain any ownership interest in any of the underlying mortgages. The Trust, then, is as its name states a Conduit where money flows in from the person who pays their mortgage and out to the investor as a payment. The right to receive those payments was purchased when the security (stock or bond) to the trust was purchased. Proceeds from that went back to the SPV who used them to purchase the mortgages from Bank A. It is a giant figure 8 circular flow of money with the Trustee coordinating it all.

Lets see who OWNS the mortgage then:The first owner was Bank A who took interest in the property as collateral on its loan to Caprice. Simple enough. When Bank A sold the mortgage to the SPV its interest was extinguished. Ownership of the promissory note WAS transferred to the SPV who is now the note holder. The SPV forms the REMIC trust and transfers the note into the trust, thereafter it irrevocably changes the nature of Caprice's mortgage. It becomes a Security. Once again, the SPV must transfer the note and pay taxes on the transfer. The mortgage now in the trust becomes for all purposes a blended group of monthly payments. These payment streams become the source of funds that the trustee pays out to investors. In essence the trustee—when certificates, stocks or bonds to the trust are sold—sells abeneficial interest in the mortgage. That is not ownership of any portion or any segment of the revenue stream but rather is simply a security—just like a share of IBM or Google doesn't entitle you to any of the assets of the company. But who owns the note?Because of the tax exemption of the REMIC it is PROHIBITED from retaining any ownership of the underlying assets it no longer holds any ownership to the note on the day it is formed. The investors in the trust do not hold any interest in the note either, they only hold the security which was sold to them. So what happened to ownership of the note? It was EXTINGUISHED when it entered the trust in order to obtain the flow of cash back to the original lender and the tax-preferred investment proceeds to the investors. So, who does Caprice owe the money to? Who has authority to release the deed to Caprice when her mortgage has been satisfied? The answer? No one.

The trust is set up and cannot take an active role in the collection of the funds. It is a shell entity ONLY. Therefore it appoints a servicer to collect the payments every month. The servicer (Bank) is hired by the trustee (Another Bank) to process incoming payments. A portion of that compensation is also any fees that are generated. They (the Servicer) only serve as a collector function. When a Servicer acts as an agent in the foreclosure process the Servicer must present affidavits that they are the owner of the note--something they cannot legally do because their only relationship is derived from the trust (which also retains no ownership in the note).

So what happens when Caprice defaults? How is his property foreclosed upon?In this proceeding the Servicer presents documents to the court (or the trustee of the deed in a non-judicial foreclosure state) that state that THEY are the owner of the note and have a legal standing to foreclose. This is not true, is not legally possible, and is fraudulent. The servicer is the agent of the Trust and will use that to claim that they are foreclosing on behalf of the trust. The problem? The Trust itself cannot hold ownership of the note because of its tax-preferred REMIC status! What about if they state that they are representatives of the investors? The investors have no ownership interest in the underlying mortgages, they only have ownership interest in the securities that were issued to fund the trust! So who does Caprice owe? The answer is nobody. The process of a note becoming a Security is final and irreversible. You cannot unscramble the eggs. A Security cannot be used to foreclose. The Kansas Federal Court Ruling decided once a note was securitized it was no longer a note and would NEVER be a note again. It becomes a Security. (Landmark National Bank v. Kesler, 2009 Kan. LEXIS 834.)Bottom Line -All Terms of Your Mortgage Were Fulfilled:The Lender was paid from the SPV upon selling the note.

The SPV was paid from the Trustee who received money from the sale of securities.

The Servicer was paid on schedule by the Trustee from fees generated.Owners of the certificates (bonds or stock) received a payment from the Trust.The REMIC Trust itself was insured by the SPV to protect investors.If the terms of the mortgage were fulfilled (i.e. everyone was paid) To Whom Does Caprice Owe Any Money? Here is an actual lawsuit filed against REMICsThere still exists a lien on the house that is unenforceable. You would have to go through a process to extinguish that lien by having an attorney file for you a Quiet Title, that silences or quiets any more claims to the property